The bottom line first: More than three‑and‑a‑half years into this bull market, the core principles of long‑term investing remain just as relevant. Historically, markets have rewarded those who stay diversified, avoid reactive decisions, and keep their focus on long‑term financial goals.

It has now been more than three‑and‑a‑half years since the bull market began in October 2022. At that time, inflation was rising at its fastest pace in fifty years, the Fed was hiking interest rates, and ChatGPT was still a month away from being released to the public. Since then, the S&P 500 has more than doubled in value.

Although the world has changed since then, the fact that there are market concerns in the headlines has not. Each cycle brings new challenges and questions about whether the tried‑and‑true rules of investing are still relevant. The reality is that each cycle is unique, with catalysts, innovations, and sources of uncertainty that are never quite the same. And yet, the underlying principles of investing and financial planning have remained consistent across decades and have continued to point people in the right direction this year.

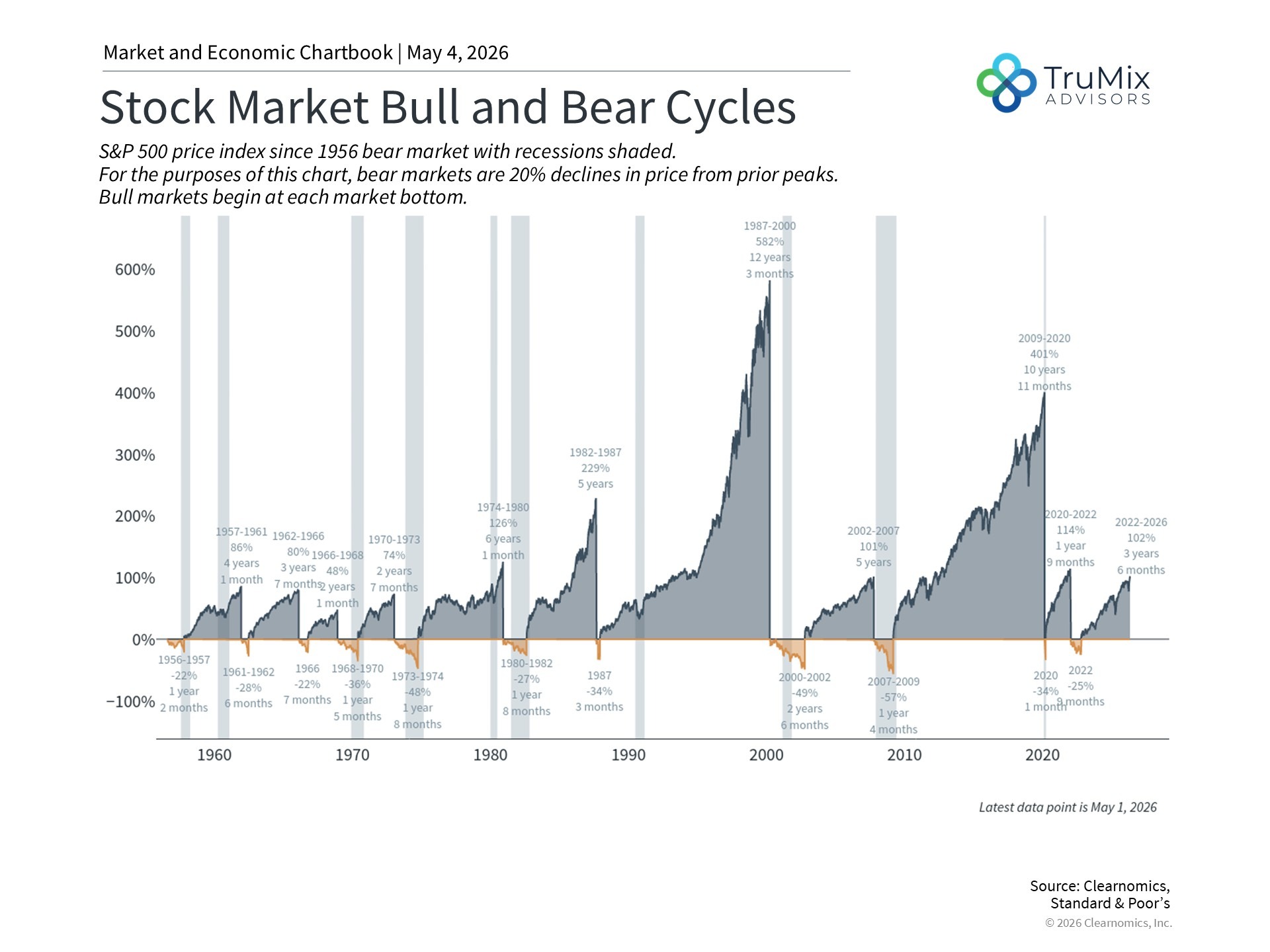

Bull markets climb a wall of worry

Even though geopolitics continue to impact markets, perhaps the more important consideration for long‑term planning is the overall market cycle. With the market hovering near all‑time highs, it’s natural for people to worry about market pullbacks and corrections. After all, these events can occur frequently, with the S&P 500 historically experiencing four or five pullbacks of 5% or worse each year, on average.1 While they are never pleasant, long‑term progress depends much more on historical patterns that play out over years and decades.

This is one reason overreacting to short‑term market swings can be counterproductive, since it may leave people poorly positioned relative to their long‑term financial goals.

You might have heard the phrase that the market climbs a “wall of worry.” Over the past several years, markets have pushed through high inflation, a banking crisis in 2023, geopolitical conflicts, the possibility of a Federal Reserve policy misstep, AI‑driven market concentration, tariff‑related volatility, and more. None of these concerns are trivial, and yet through all of them, markets have continued to move higher.

The chart above illustrates this pattern starting from World War II. Over this 70‑year period, bull markets have lasted far longer and generated significantly larger gains than what has been lost during bear markets. Bear markets have typically lasted one to two years on average, while recent bull markets have extended ten years or more. Even when corrections occur during bull markets, the average decline has been around 14%, with recoveries taking just a few months on average.2

One example is the bull market that followed the 2008 financial crisis, which lasted nearly eleven years. Despite its strong performance, it’s often referred to as “the most unloved bull market,” given the steady stream of economic and market concerns throughout the cycle. Looking back, it’s clear that—even when those concerns were valid—they didn’t justify abandoning long‑term plans.

Of course, the past is no guarantee of future results, and recovery timelines vary by circumstance. Still, history consistently shows that reacting to every market movement has often caused people to miss a meaningful portion of the gains that followed.

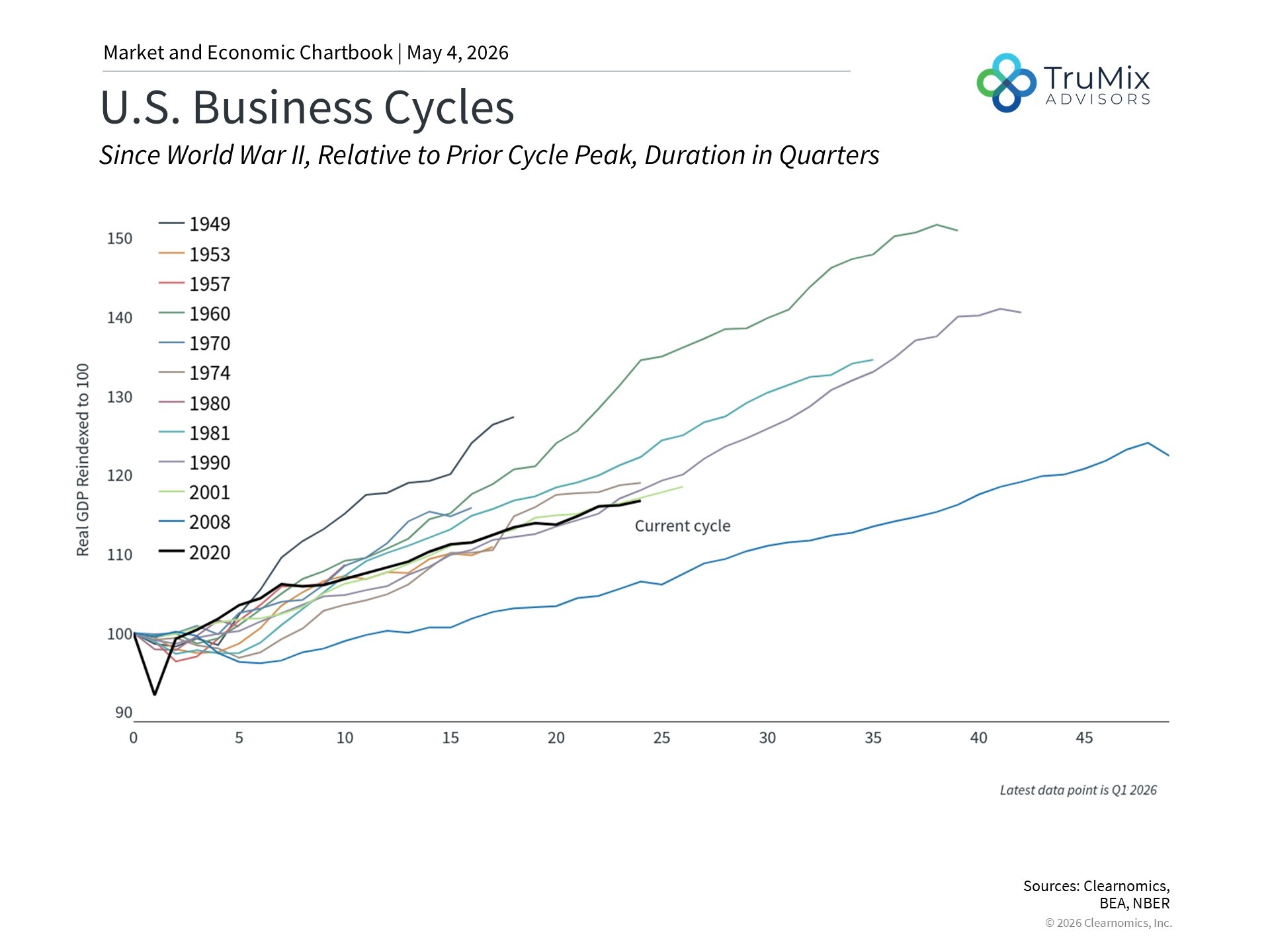

A growing economy is the foundation for long‑run returns

While the stock market and the economy are not the same thing, they are closely connected. Over time, corporate earnings drive stock prices, and those earnings ultimately depend on economic growth. This is why it’s important to keep an eye on the broader economic cycle, even as markets move day‑to‑day for many other reasons.

The current business cycle has technically been running about two‑and‑a‑half years longer than the market cycle. The most recent official recession, as determined by the National Bureau of Economic Research, was the brief but sharp contraction during the pandemic in 2020. Since then, periods of slower growth and repeated recession predictions have surfaced—but none have materialized.

Today, the economy remains healthy by many measures, even as people watch three areas closely. First, sustained oil prices above $100 per barrel could weigh on consumer spending and add inflationary pressure. Second, the job market has cooled, particularly in technology, raising questions about consumer behavior. Third, the scale of AI investment has prompted concerns about a potential bubble—a natural response for those who lived through the dot‑com bust or the housing crisis.

Bubbles are notoriously difficult to identify in real time, and history shows that high valuations don’t always end in sharp declines. So far in this cycle, earnings growth has supported valuations, and many businesses are funding expansion through profits rather than debt. For long‑term planning, the key is staying diversified across different areas of the market—maintaining exposure to growth while managing risk.

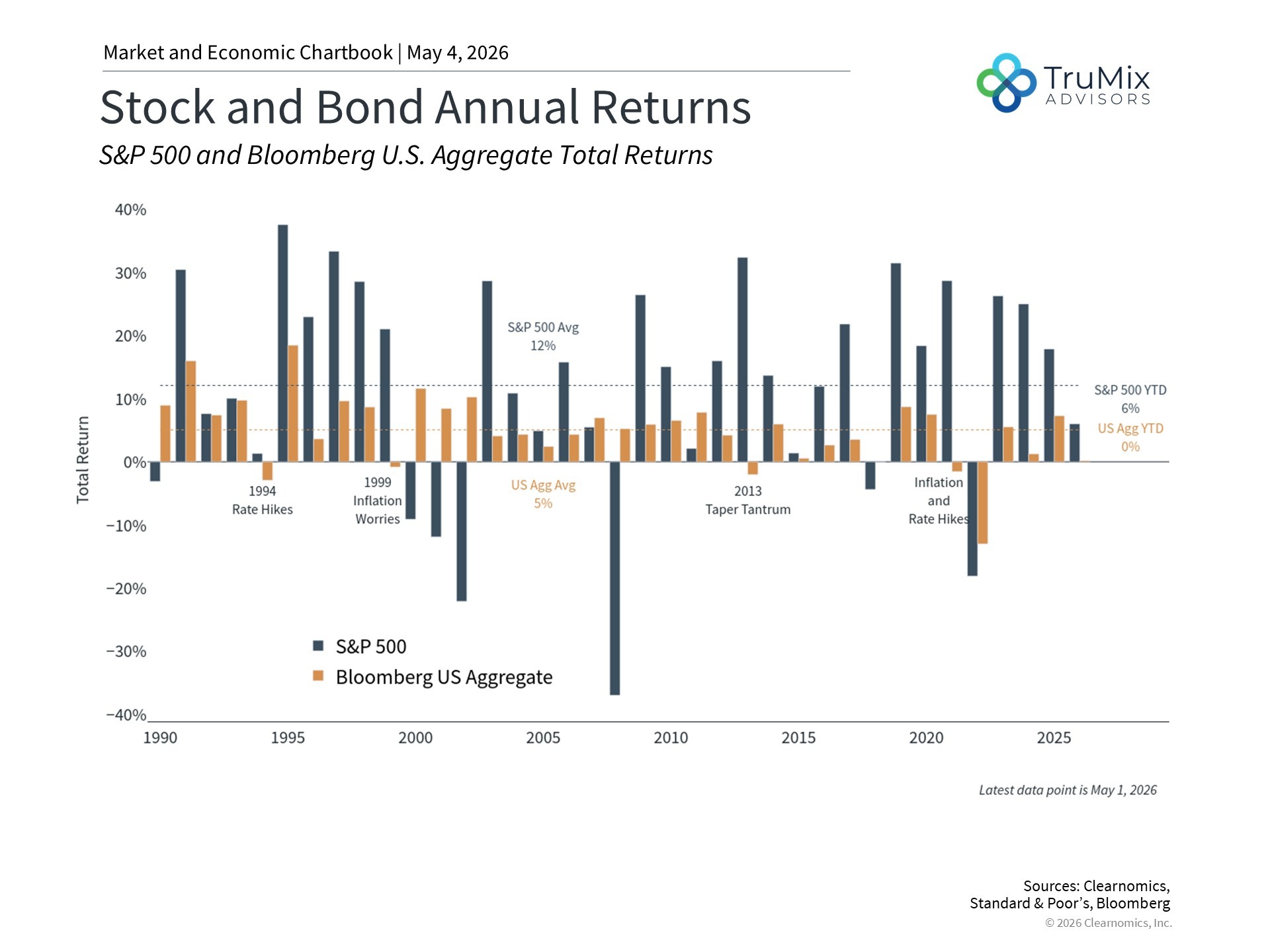

Stocks and bonds continue to work together

Every market cycle raises questions about whether long‑standing portfolio principles still apply. In 2022, when both stocks and bonds declined amid rapidly rising rates, many people questioned whether bonds still played a meaningful role in diversified portfolios. Similar doubts surfaced after the 2008 financial crisis, when bond yields remained historically low for years.

In recent years, bonds have not only recovered but have resumed providing income and balance. The Bloomberg U.S. Aggregate Bond Index has posted positive returns in each of the past two years, helping smooth periods of stock market volatility. International stocks and commodities have also contributed, reinforcing the benefits of diversification.

This pattern aligns with history. Each era brings a belief that “this time is different.” In the 1970s, inflation dominated. During the dot‑com era, technology stocks captured outsized attention despite limited profits. In 2022, rising rates pressured both stocks and bonds simultaneously. Today echoes elements of each of those periods.

Time and again, focusing on diversification and long‑term planning has proven effective. As uncertainty persists and headlines shift, keeping a bigger‑picture perspective remains critical.

Footnotes & Sources:

1. The number of pullbacks is based on S&P 500 index price returns since 1980.